BOOM! Mercom Capital Group published their Q4 and 2020 roundup of global digital health investment and, no surprise, the investment picture for just about anything digital health was in sharp contrast to most of the COVID-afflicted world economy.

The topline:

The topline:

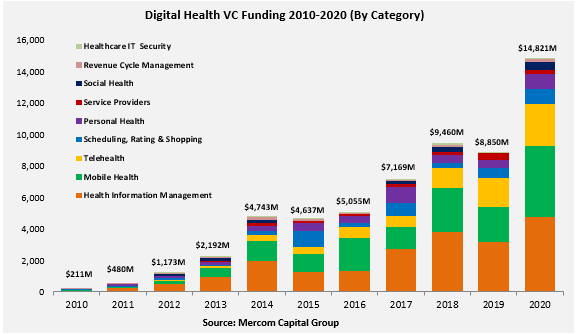

- Global VC funding (private equity and corporate venture capital) was $14.8 bn across 637 deals. It was a 66 percent increase in funding compared to 2019’s $8.9 bn in 615 deals. The modest increase in deal number and huge increase in funding points to the acquisition of more established companies requiring Big Deals.

- Total corporate funding, including VC, debt, and public market financing, totaled $21.6 billion

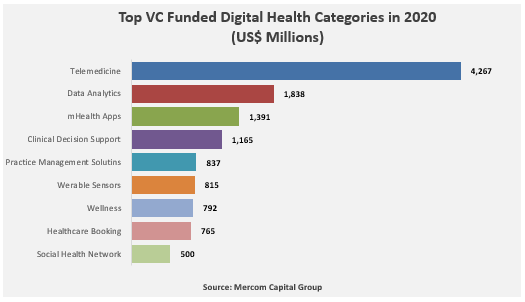

In a stunning change, telemedicine was Top Of The Pops, with $4.3 bn in  investment, 139 percent over 2019’s $1.8 bn. It was over double the former star categories of data analytics and mHealth apps.

investment, 139 percent over 2019’s $1.8 bn. It was over double the former star categories of data analytics and mHealth apps.

The top five disclosed M&A transactions in 2020 they tracked were:

- Teladoc’s acquisition of Livongo Health for $18.5 bn

- Blackstone’s acquisition of a majority stake in Ancestry.com for $4.7 bn (despite the ‘bloom off the rose’ of consumer genetic testing)

- Philips’ acquisition of BioTelemetry in cardiac monitoring for $2.8 bn

- Invitae’s acquisition of ArcherDX for $1.4 bn

- WellSky’s acquisition of Allscripts’s CarePort Health (CarePort) for $1.35 bn

The Executive Summary is available for free download at the link in the release. The full report will set you back $599 – $999, depending on the version.

StartUp Health has slightly different numbers but in total investment tracks almost to Mercom Capital’s estimate at $21.5 bn. For telemedicine, it still triples year-over-year but StartUp’s totals are lower: 2019’s $1.1 bn to 2020’s $3.1 bn. Part of the difference may be remote monitoring, which StartUp considers separately. It doubled from $417 million to $941 million. Their deal counts were also higher: 764 in 2020 compared to 716 in 2019. Another fun fact in their tracking are their city leaders in health innovation funding: Beijing, Tel Aviv, and London, confirming that New York and the San Francisco metro no longer have money, interest, or their former attraction. A fuller list would have been interesting. More is in their Part 1 study. Part 2, to be released next week, will cover their dozen ‘health moonshots’.

Most Recent Comments