Baby monitoring system Owlet closed its SPAC late last week with Sandbridge Acquisition Corporation. It is now trading on the NYSE (OWLT) for around $8 per share. With Sandbridge’s investment and the concurrent private placement (PIPE), Owlet now has $135 million and a valuation of over $1 billion, far exceeding the $325 million estimated [TTA 17 Feb]. Owlet started in 2013 with a ‘Smart Sock’ (right) at $299 using pulse oximetry to monitor baby heart rate, oxygen levels, and sleep patterns with readouts via their app, but has expanded to include an Owlet Cam and a Dream Lab to encourage good baby sleep, which parents will be the first to appreciate. Mobihealthnews

Baby monitoring system Owlet closed its SPAC late last week with Sandbridge Acquisition Corporation. It is now trading on the NYSE (OWLT) for around $8 per share. With Sandbridge’s investment and the concurrent private placement (PIPE), Owlet now has $135 million and a valuation of over $1 billion, far exceeding the $325 million estimated [TTA 17 Feb]. Owlet started in 2013 with a ‘Smart Sock’ (right) at $299 using pulse oximetry to monitor baby heart rate, oxygen levels, and sleep patterns with readouts via their app, but has expanded to include an Owlet Cam and a Dream Lab to encourage good baby sleep, which parents will be the first to appreciate. Mobihealthnews

Carbon Health, which is certainly an odd name for a primary care provider plus virtual health with a streamlined patient record/EMR system and makes insurers happy because they charge only Medicare rates, received a hefty $350 million Series D raise. Led by Blackstone Horizon Partners with Atreides, Homebrew, Hudson Bay Capital, Fifth Wall, Lux Capital, Silver Lake Waterman, and BlackRock participating, along with returning investors Dragoneer Investment Group and Brookfield Technology Partners along with a slew of private investors, it follows on last November’s Series C of $100 million for a total raise since 2016 of $522 million. Valuation is what used to be an eye-blinking $3.3 billion. Carbon’s locations are a bit strange–concentrated in California and SF area with outposts, many of which are limited service or ‘pop-ups’, in Florida, Arizona, Kansas, and NYC. Unlike the recently covered One Medical, it does not require any kind of annual concierge fee. The model is an interesting one in positing high service and low cost. The founders are also staking out becoming the largest US primary care provider, which Village Medical or UnitedHealth Group would not be delighted about. One wonders if all this staking out will work, or is to attract payer investment when the VCs decide to exit. FierceHealthcare, Mobihealthnews (referring to them as multimodal, which sounds like ocean/rail transport or articulated lorries), Forbes

Also in the Mobihealthnews article: a Series B $90 million raise by Woebot Health, developer of a mental health chatbot (ok, relational agent), and the $32 million Series B raise of b.well Connected Health, a patient-facing health management platform that will get a big boost from interoperability around patient records required under the Cures Act. Woebot’s twee infographic about their therapeutic bond study in the JMIR is woeful, though, as large parts are unreadable.

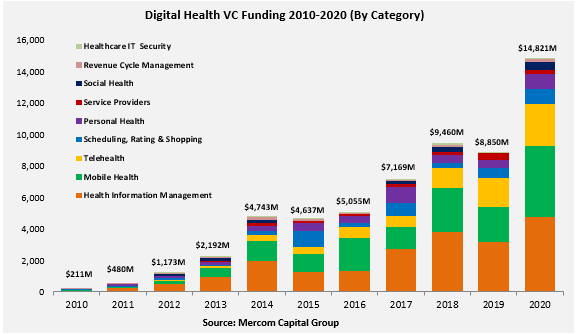

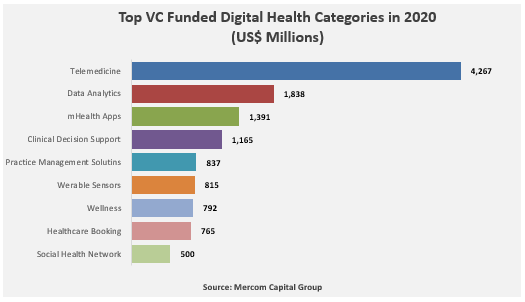

No surprise that digital health funding hit a $15 billion high in the first half of 2021, up 138%, driven in large part by telehealth investment. This is based on a report from Mercom Capital Group. FierceHealthcare

Most Recent Comments